Up to $20K of Student Loan Debt Cancelled for Millions

On August 24th, President Joe Biden unveiled his three-part plan to reduce student loan debt, which includes extending the pandemic-related payment moratorium, student loan forgiveness, and a new income-based repayment plan.

Student Loan Forgiveness

In order to facilitate the transition back to repayment and support borrowers who are most at risk of delinquencies or default once payments resume, President Joe Biden announced the long-awaited federal student loan forgiveness program, which includes up to $20,000 in forgiveness for tens of millions of borrowers.

Do I qualify for forgiveness?

Your annual income must be less than $125,000 (for individuals) or $250,000 (for married couples or heads of households) to qualify for forgiveness.

- If you received a Pell Grant while in college and your income is within the threshold, you are eligible for up to $20,000 in debt forgiveness.

- If you did not get a Pell Grant while in college and your income is within the threshold, you are eligible for up to $10,000 in debt forgiveness.

Federal Parent Plus loans are also eligible for loan forgiveness if the parents meet income thresholds.

Loans held by currently enrolled college students may be forgiven under this program. Any loans disbursed before June 30, 2022, are eligible for loan forgiveness. Borrowers who are dependent students will qualify for relief based on their parent’s income.

When can federal student loan borrowers expect loan forgiveness?

Approximately 8 million borrowers who enrolled in the income-driven payment plan could receive automatic relief because the U.S. Department of Education already has access to relevant income data needed to get qualified for relief..

The majority of federal student loan borrowers who meet the income standards must submit an application in order to be forgiven their debt. The Administration expects to release the application by early October. After submitting their application, borrowers could receive relief in 4-6 weeks.

Borrowers are encouraged to apply before November 15 in order to receive relief before the payment pause ends on December 31, 2022.

In the meantime, you can sign up through the Department of Education’s subscription page to get notifications when the application form is made accessible and the loan forgiveness process begins. The Federal Student Aid website states that the application deadline is December 31, 2023.

Is the forgiven student debt taxable?

In general, when a debt (including student loans) is forgiven, waived, reduced, or canceled, the borrower can be required to pay taxes on the canceled balance as if the canceled debt was “income” received by the borrower during the year that the cancellation took place.

However, due to the American Rescue Plan Act (ARPA), which was put into law in 2021 during the COVID-19 pandemic, forgiven student debt is not subject to federal income taxes until the end of 2025.

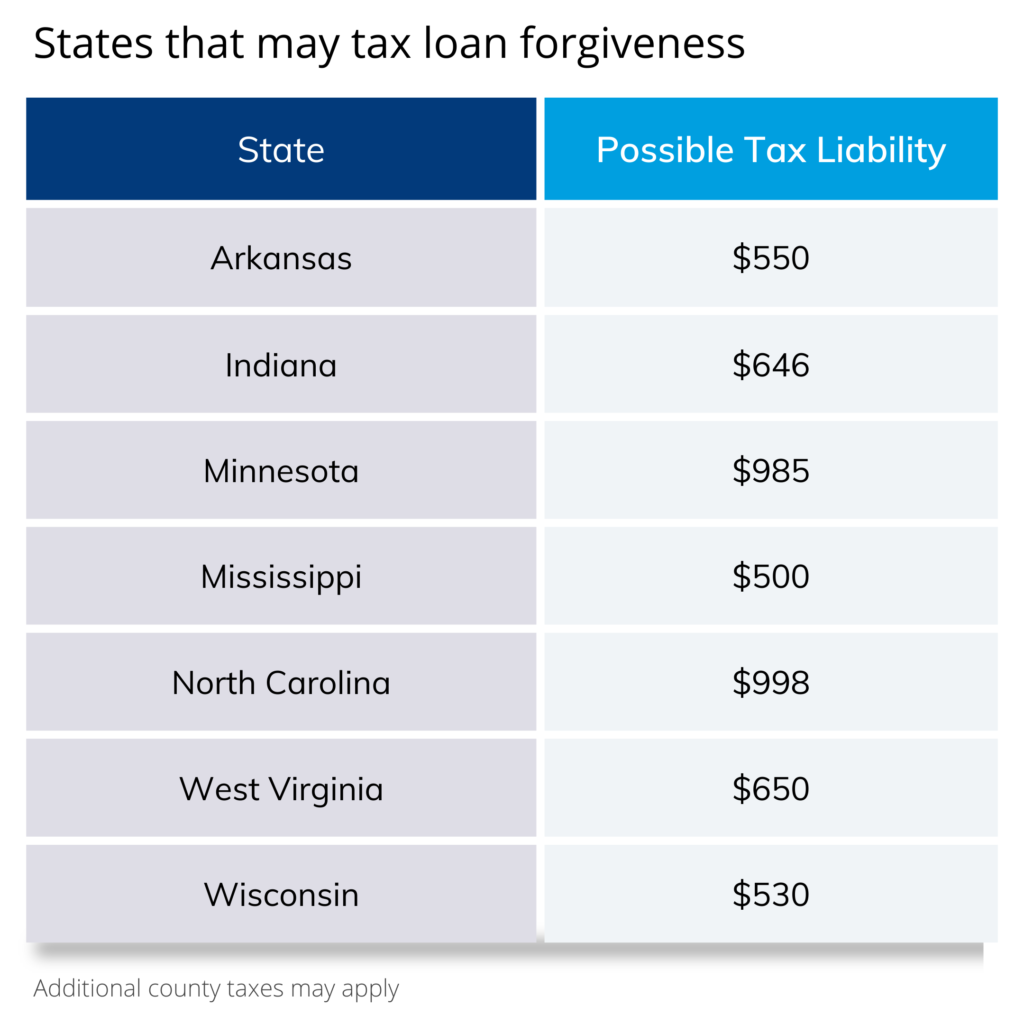

Most states automatically follow federal regulations, other states may consider the forgiven sum to be income, so it’s still possible that you’ll owe taxes.

These 6 states could tax your loan forgiveness; Arkansas, Indiana, Minnesota, Mississippi, North Carolina, West Virginia, and Wisconsin.

Extended Student Loan Payment Pause

The Biden-Harris Administration will extend the repayment pause through December 31, 2022, with payments beginning in January 2023, in order to ensure a smooth transition to repayment and avoid unneeded defaults.

Refunds for Payment Made During Pause

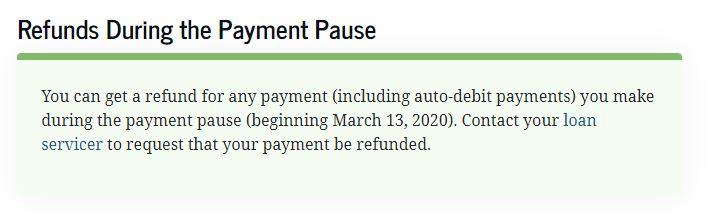

The federal student loan repayment moratorium, which has been in effect since March 2020, has spared student loan borrowers from making loan payments or accruing further interest.

However, some took advantage of the situation to pay off their principal and make progress on their debts. Now, it appears they would be qualified to receive a refund for any payments made during the pause.

The Federal Student Website states that “You can get a refund for any payment (including auto-debit payments) you make during the payment pause (beginning March 13, 2020). Contact your loan servicer to request that your payment be refunded.”

Although some people have already asked their servicers for refunds, you may want to wait until the Department of Education releases more information to fully understand how payments made during the pandemic will affect overall balances and eligibility for student loan forgiveness. Here is a list of the federal student loan servicers.

New Income-Driven Repayment Plan

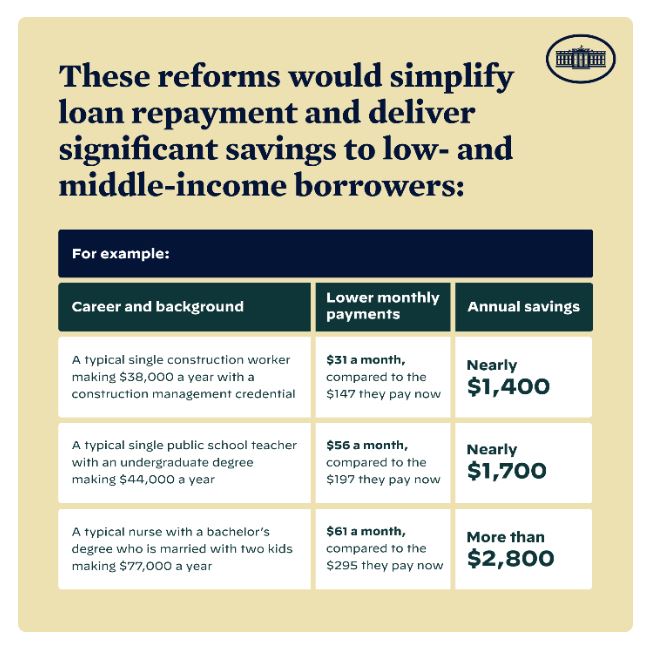

The U.S. Department of Education has long offered income-based repayment options. However, a new income-driven repayment plan will significantly lower future monthly payments for borrowers with lower and moderate incomes.

In the current “income-driven repayment” plans, borrowers typically pay 10% of their discretionary income annually for up to 20 years; any remaining debt is then discharged (although after 2025, they will be required to pay taxes on the discharged amount, which the Internal Revenue Service will classify as income).

In order to reduce the cost of loan repayment for borrowers in the income-driven repayment program, the administration proposed rules that would:

- Limit the amount of discretionary income that students may use to repay their undergraduate debts to no more than 5% each month.

- Raise the threshold for “non-discretionary” income exempt from repayment such that no borrower earning less than 225% of the federal poverty level (about the annual equivalent of $15 minimum wage for a single borrower) will be required to make a monthly payment.

- For borrowers with loan balances of $12,000 or less, loans will be forgiven after 10 years of payments rather than 20.

- Cover the borrower’s outstanding monthly interest so that no borrower’s loan debt will increase as long as they make their monthly payments, even if that monthly payment is $0 because their income is low, unlike other existing income-driven repayment plans.

Eco-Tax, Inc: Virtual Tax Consulting Service

Eco-Tax offers affordable tax planning and preparation packages. When working with Eco-Tax, you will be paired with an experienced CPA (certified public accountant) or EA (licensed enrolled agent) tax consultant who are experts in both your industry and your state. Your dedicated tax consultant will be your trusted advisor providing you support year-round.

Get in touch at 866.968.4848 or complete our online free consultation form. One of our experts will respond shortly!