States Pass Elective PTE Tax: A Workaround for the SALT Cap

Several states have enacted elective pass-through entity taxes as a workaround to the federal cap on individuals’ state and local tax deductions. When a pass-through entity tax is chosen, the tax is applied to the entity rather than the owners directly. Generally, qualifying pass-through entities include entities taxed as S-Corporations and Partnerships; some states also include sole proprietors, and LLCs taxed as disregarded entities.

Why did states enact the pass-through entity tax?

The Tax Cuts and Jobs Act of 2017 (TCJA) imposed a $10,000 cap on individual itemized deductions for state and local sales, income, and property taxes (SALT) for tax years 2018 through 2025, as well as SALT deductions for trusts and estates. In response to the TCJA’s SALT tax cap, many states have enacted a pass-through entity (PTE) tax, which allows business owners to elect to have their PTE pay state and local income taxes at the entity level rather than at the individual level. In November 2020, the Internal Revenue Service (IRS) issued Notice 2020-75, confirming that state taxes paid through a PTE are exempt from the SALT cap. Now 24 states have enacted an elective PTE tax which has been shown to be effective.

What is an elective pass-through entity tax, and how does it work?

The PTE tax election allows state and local income tax to be imposed on a PTE rather than its partners, members, or shareholders. The entity can then deduct those income taxes in their entirety for federal tax purposes. The partners, members, or shareholders will either receive a credit against their state individual income tax liability or be able to deduct or exclude their distributive share of income from their adjusted gross income when calculating their state income tax liability.

The laws governing tax elections for pass-through entities differ significantly from state to state. The following is a basic explanation of how the PTE tax elections work:

- The PTE tax election is primarily available to businesses taxed as S-Corporations and Partnerships. In certain states, sole proprietorships, business and statutory trusts can also elect an entity-level tax.

- The election is made annually. In some states, once the election is made for a particular tax year, it is irrevocable for that year. In other states, the election cannot be modified for a number of years.

- In many states, the entity can make an election up until the due date for submitting the business’s tax return, including extensions. In other states, an election must be made no later than the 15th day of the fourth month after the end of the tax year for which the entity has elected to be taxed at the entity level. Connecticut is the only state that requires pass-through entities to pay an entity-level tax.

- The election in some states is made using a specific form. You can make an election on a timely filed return in other states.

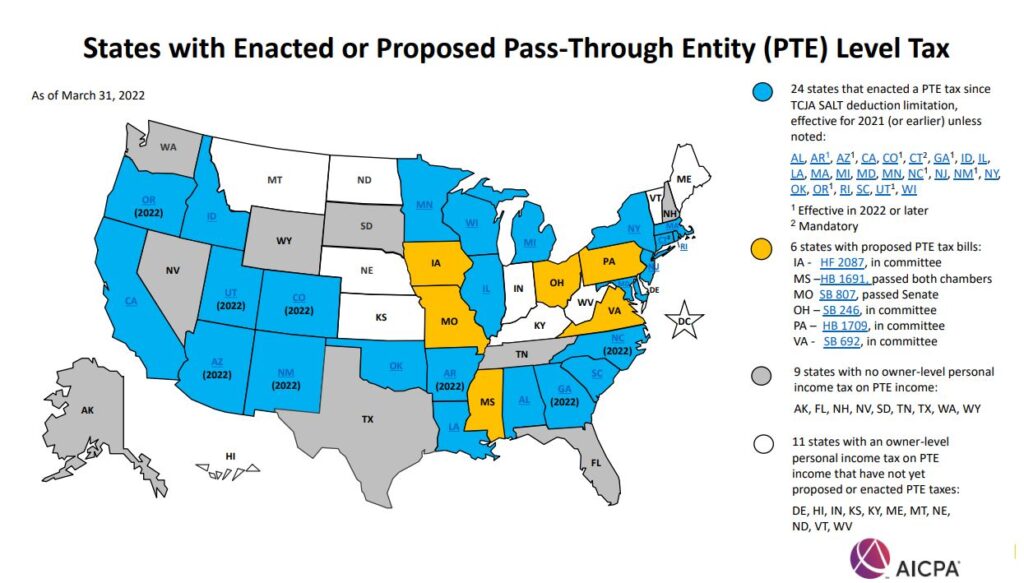

Which states have enacted pass-through entity tax?

The map below shows the states that have enacted PTE tax legislation. Connecticut is the only state with a mandatory PTE tax. All the other 23 states that have passed the bill require a PTE election, which include Alabama, Arkansas, Arizona, California, Colorado, Connecticut, Georgia, Idaho, Illinois, Louisiana, Massachusetts, Michigan, Maryland, Minnesota, North Carolina, New Jersey, New Mexico, New York, Oklahoma, Oregon, Rhode Island, South Carolina, Utah, and Wisconsin. In 2022, six more states are projected to pass PTE tax legislation, including Iowa, Mississippi, Montana, Ohio, Pennsylvania, and Virginia.

Pass-Through Entity Tax Chart

| State | Effective Date |

| Alabama | January 1, 2021 |

| Arizona | January 1, 2022 |

| Arkansas | January 1, 2022 |

| California | January 1, 2021 |

| Colorado | January 1, 2022 |

| Connecticut | January 1, 2018 |

| Georgia | January 1, 2022 |

| Idaho | January 1, 2021 |

| Illinois | January 1, 2021 |

| Louisiana | January 1, 2019 |

| Maryland | January 1, 2020 |

| Massachusetts | January 1, 2021 |

| Michigan | January 1, 2021 |

| Minnesota | January 1, 2021 |

| NorthCarolina | January 1, 2022 |

| New Jersey | January 1, 2020 |

| New Mexico | January 1, 2022 |

| New York | January 1, 2021 |

| Oklahoma | January 1, 2019 |

| Oregon | January 1, 2022 |

| Rhode Island | January 1, 2019 |

| South Carolina | January 1, 2021 |

| Utah | January 1, 2022 |

| Wisconsin | January 1, 2018 |

Is the state PTE tax election right for your business?

In most cases, making a PTE tax election will benefit the owners; nevertheless, this is not always the case. The legislation governing these entity-level tax elections varies substantially from one state to the next. Analysis will be required because each state has its unique set of norms. Regardless of where a PTE operates or where the owners live, before making a decision, examine the following questions:

- In each state, what types of owners are allowed to make an election?

- Does making the election benefit some owners and not others?

- Will making the election result in the loss of other state tax benefits?

- Is there an alternative minimum tax in place in your state that caps the amount of tax relief you can get?

- Is it possible to make a PTE tax election in every state where the organization does business?

- Is it possible to claim a credit for taxes paid to other jurisdictions in the state where the individual resides?

How we can help

Before deciding to make a PTE tax election in one of the states that now allow it, you should carefully consider the dynamics of different owners in the PTE, as well as the differences in state rules. Our tax experts can assess your situation and investigate the potential benefits of a PTE tax election. Please contact us if you need help deciding whether a PTE tax election is right for your company or if you have any questions. To learn more about how we can help you book a free consultation with one of our trusted advisors.