How to Calculate Cryptocurrency Taxes

As the cryptocurrency market continues to grow the IRS has increased its efforts to increase cryptocurrency tax compliance. If you have bought cryptocurrency or are interested in buying there are a few things you should know regarding cryptocurrency taxation.

What is Cryptocurrency?

Cryptocurrency is a virtual currency that uses crypto technology to secure payment online. Unlike fiat currency, it is not issued by a central authority. Its decentralized nature makes it immune to government interference.

There are thousands of cryptocurrencies available to more mainstream individuals and institutional investors. There are also many new online platforms that facilitate trading cryptocurrencies.

Some of the biggest cryptocurrencies include Bitcoin (BTC), Ethereum (ETH), Binance Coins (BNB), Cardano (ADA), and Tether (USDT) based on market capitalization.

Rapid surges in the value of the cryptocurrency has made it headline news. Now more investors are turning to cryptocurrency markets hoping to make money quickly.

The IRS has also shifted its attention to cryptocurrency. Regulators are catching up to investors that are not complying with tax reporting.

How is cryptocurrency treated for tax purposes?

Under Notice 2014-21 the IRS declared that virtual currency is treated as property for federal tax purposes. It is considered an investment similar to real estate, stocks or bonds, which are all capital assets.

When selling a capital asset you pay either short term or long-term capital gains tax on the realized profits. The taxable gain on the sale of the cryptocurrency is the difference between the purchase price (cost basis) and the sale price.

The tax rate applied depends on the length of time the cryptocurrency was held and your income. When held less than a year it is treated as short term capital gains which are taxed at the ordinary income tax rate ranging from 10%-37%. Cryptocurrency held for more than a year is subject to lower long term capital gains tax of 0%, 15%, or 20%.

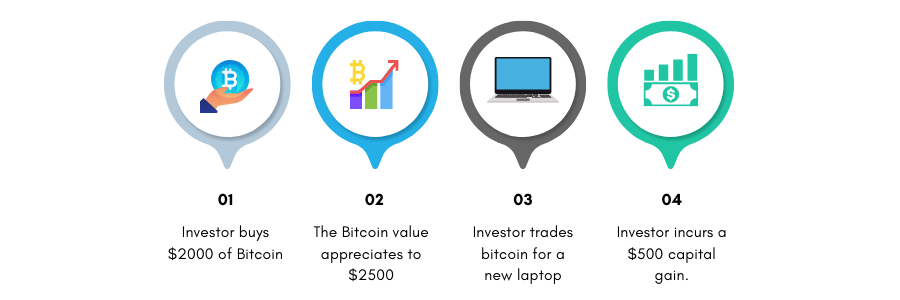

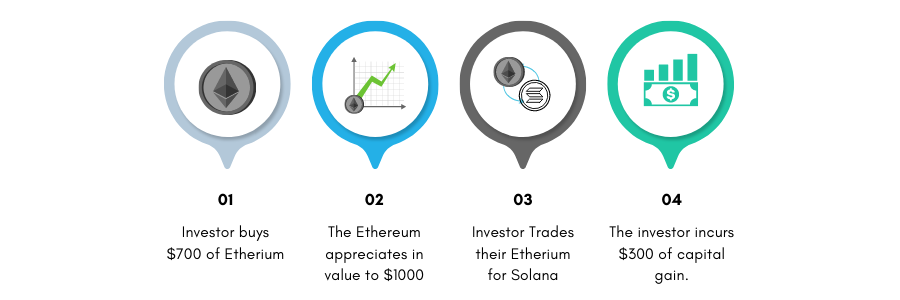

When cryptocurrency is exchanged for other property, goods or services the investor must realize a gain or a loss. The taxable gain realized in the exchange is the difference between the fair market value of the property received and the cost basis of the cryptocurrency.

What is a taxable event?

A cryptocurrency transaction that results in a realized gain, such as:

- Selling cryptocurrency for fiat currency (cash)

- Receiving goods or services in exchange for cryptocurrency. As well as receiving cryptocurrency as payment for goods or services.

- Trading one cryptocurrency for another cryptocurrency.

- Mining for cryptocurrency (the mined coins fair market value on the day it was mined is taxable income)

What are the tax implications of donating, gifting, or inheriting cryptocurrency?

- Cryptocurrency Donations- are treated like cash donations and are tax deductible. At the time of the donation the fair market value of the cryptocurrency is assigned.

- Cryptocurrency Gifts- that are below $15,000 are not taxable. If the gift is sold then the cost basis is the same as the donor’s.

- Cryptocurrency Inheritance- follows the same rules as other estate assets. The crypto asset receives a step-up basis to the fair market value at the time of death.

What are tax reporting requirements?

You are required to report virtual currency transactions on your income tax returns. Any amount of profit must be reported. You must also keep records of all transactions, buying, selling, or usage of virtual currency.

Failure to report can result in an IRS Audit. In the most extreme cases, tax evasion could lead to criminal charges and fines as high as $250,000.

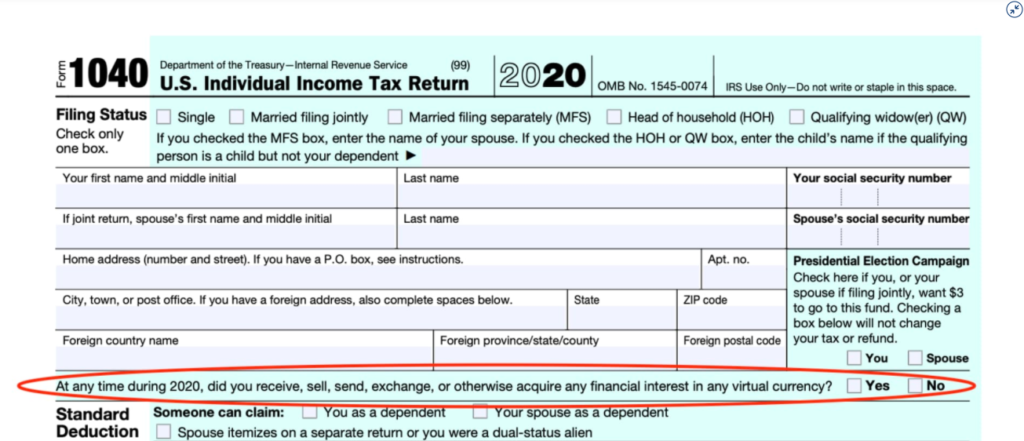

For tax year 2019 the IRS asked taxpayers for the first time if they had virtual currency transactions on Schedule 1 of tax returns. In 2020 the IRS improved their strategy by moving the question to the first page of the 1040 tax return (question:“ At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency?).

The IRS continues to increase its efforts to ensure all taxpayers comply with reporting requirements of these transactions. It is aggressively seeking cases of tax evasion.

In 2019 the IRS sent letters to 10,000 taxpayers that were suspected of failing to report their virtual currency transactions. Recently, as a way to identify individuals that conducted at least $20,000 of transactions in cryptocurrency during the years 2016-2020 the IRS has been authorized by the court to issue summons to Kraken and Circle.

If you are going to invest or have invested in cryptocurrencies you should take a close look at tax implications and consult with your advisor.

Partner with a Trusted Tax Accountant at Eco-Tax

Need help with cryptocurrency compliance? We at Eco-Tax are ready to assist you with cryptocurrency tax planning and reporting. To learn more about how we can help you, contact us today to book a free consultation with one of our trusted advisors. We look forward to partnering with you!