Tax-Smart 529 Education Savings Plans

For many families, a huge concern is finding a way to pay for their children’s college education. Especially, with the climbing cost of higher education. According to the College Board’s Trends in College Pricing and Student Aid 2020 report, the average cost of tuition in 2020-2021 was $37,650 in private colleges, $10,560 at public colleges, and $27,020 at public colleges for out-of-state residents.

- View Report on Trends in College Pricing and Student Aid

- Estimate cost with the College Cost Calculator

529 Education Savings Plan

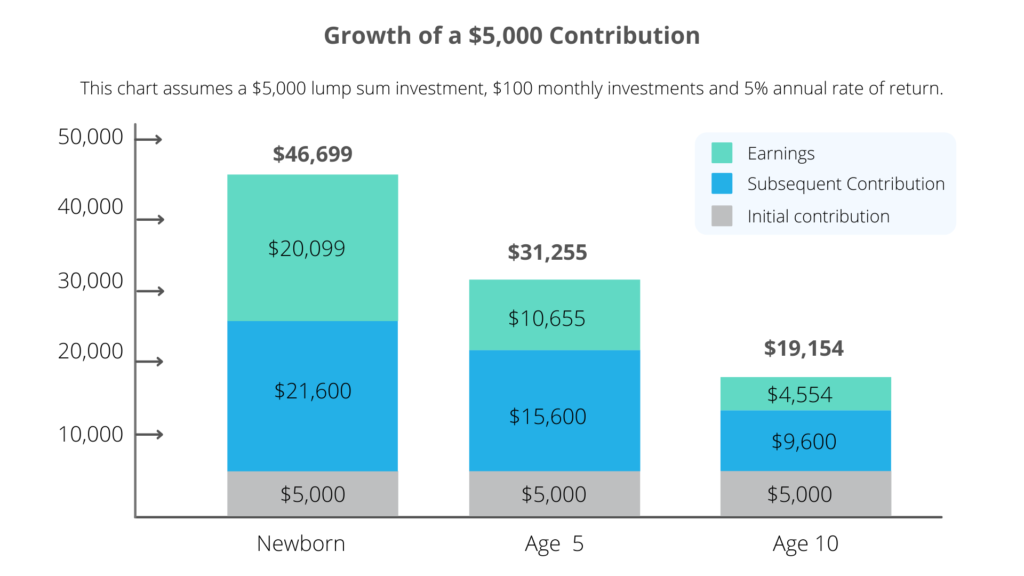

A great way to save for the cost of college expenses is to invest in a 529 Education Savings Plan which has both federal and state tax advantages. The money saved in this type of account will grow tax-free and withdrawals used to pay for qualified educational expenses are not taxed. Qualified educational expenses include tuition fees to attend eligible post-secondary educational institutions, payment for room and board, mandatory fees, books, supplies, computers, and software.

Since 2018 the Tax Cuts and Jobs Act allows families to use up to $10,000 per year to cover payment of elementary and secondary tuition expenses. In 2019 the SECURE Act expanded the allowable use of 529 distributions to cover up to $10,000 of student loan repayments. This law also allows funds to be used to pay for apprenticeship programs that are registered with the department of labor.

In summary 529 Plans can be used for the following qualified educations expenses:

- College tuition, room, and board required fees, books, and other supplies

- Up to $10,000 per year in K-12 Education

- $10,000 in student loan repayments

- Apprenticeship programs. Use this tool to find eligible apprenticeship programs.

Each 529 Plan has a designated beneficiary and an account owner. The account owner may be a parent or another person and typically is the principal contributor to the program. The account owner is also entitled to choose and change the designated beneficiary. The account owner decides who gets the funds and is legally allowed to withdraw funds at any time, subject to tax and penalties. They may change the beneficiary designation from one to another in the same family. Funds in the account roll over tax-free for the benefit of the new beneficiary.

The Prepaid Tuition Plan is another type of 529 Plan. These plans allow an account owner to purchase units or credits at participating colleges or universities for the future tuition of the account beneficiary. These plans will not cover the cost of room and board and can’t be used for K-12 tuition.

529 Information by State

529 plans are offered in every state, each state may have more than one 529 plan. Plans are sponsored by the state, state agency, or education institution. You are not required to invest in a 529 plan from your resident state although there may be a tax advantage for choosing your state’s plan.

- Find your state’s 529 Plan

- Try the 529 Search and Comparison Tool

- Browse 529 plans by state

- Check eligible institutions here

Tax Advantages

Over 30 states allow deductions or credits for contributions to 529 plans. You should review and compare state plans. Contributions made by the account owner are not deductible for federal income tax purposes. However, earnings on contributions grow tax-free. Funds used to cover qualified education-related expenses are not taxed. If 529 funds are used for a purpose other than qualified education it is taxed to the one receiving the distribution. In addition, a 10 percent penalty is imposed on the taxable portion of the distribution.

For gift tax purposes, contributions of up to $15,000 ($30,000 for married couples) per child can qualify for annual gift tax exclusion. Another option is to contribute $75,00 ($150,000 for couples) per child once every five years. Any gift above these amounts will need to be reported on IRS Form 709. However, it doesn’t necessarily mean you will need to pay gift tax. The amounts that exceed the exclusion will go against your lifetime gift exclusion of $11.7 million. Click here to view IRS frequently asked questions on Gift Taxes.

Impact on FAFSA

Generally, 529 Plans do not have a significant impact on Federal Student Financial Aid (FAFSA). Currently, parent-owned accounts have a more favorable treatment in terms of financial aid than grandparent-owned accounts. A parent-owned 529 account is considered an asset and can reduce federal financial aid by 5.64% of the account value. If the distribution is made from a grandparent-owned 529 account, then it will be considered untaxed student income and can reduce financial aid by 50% of the amount distributed. However, after new FAFSA rules are in place for the 2023-2024 school year grandparent 529 account distributions will not count towards “expected family contribution” and will have no impact on financial aid.