Retirement Plan Options

If you are self-employed or own a business, consider setting up a retirement plan if you don’t already have one. New accounts for retirement plans, such as all 401(k)plans, profit-sharing, and defined benefit plans must be established on December 31st, 2020. Many can be funded by the income tax return filing due date.

Make sure you all take the necessary steps to maximize your tax savings:

- Maximize contributions to retirement plans

- Consider establishing a Spousal IRA

- Consider Roth IRA Conversion

- Consider contributing to SEP IRA, Defined Benefit Plan, or Solo 401(k)

Let’s take a closer look at different types of retirement plans:

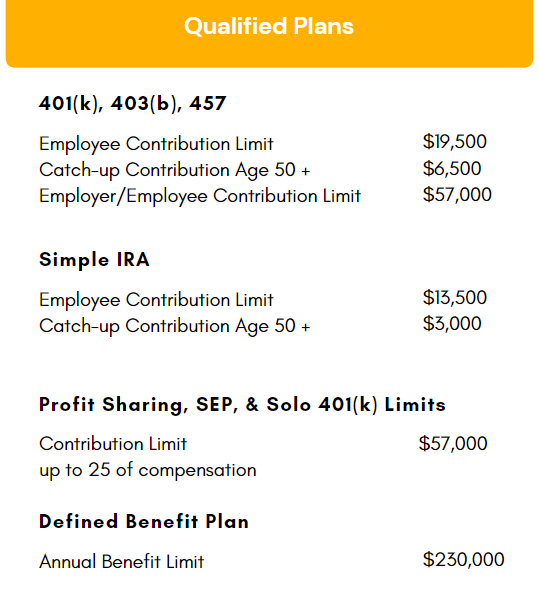

Solo 401(k)

- The Solo 401(k) is only available to self-employed or small businesses with no employees. The only exception is a spouse.

- You can make contributions as an employer and employee.

- Employee contribution is limited to the lesser of $19,500 or 100% of earned income.

- The employer portion of the contribution is limited to 25% of compensation

- The employer and employee contributions combined can’t exceed $57,000.

- Employee contribution must be made by December 31st.

- The employer portion of the contribution can be made by the due date of the federal income tax return.

SEP IRA

- The Simplified Employee Pension (SEP) Plan is for self-employed individuals and for small businesses with few employees.

- Contributions must be made to each qualifying employee SEP. However, you are not required to make one every year.

- Employers can contribute up to the lesser of $57,000 or 25% of compensation for the first $285,000.

- The contribution must be the same percentage of salary for each eligible employee.

- SEP contributions can be made until the federal income tax return filing due date

SIMPLE IRA

- The Savings Incentive Match (SIMPLE) Plan is for small business with up to 100 employees

- Employees and Employers can contribute to the plan.

- The employee contribution limit is $13,500. The catch-up contribution for those over age 50 is $3,000.

- An employer can match contributions up to 3% of employee compensation or at 1% for no more than 2 out of 5 years. Employers can also elect to have a fixed 2% non-elective contribution to each eligible employee.

- Employee’s contributions must be deposited to their SIMPLE IRAs with-in 30 days after the end of the month when the employee would have received payment. For self-employed individuals, the deposit must be made no later than January 30th or 30 days after the end of the year.

- Employer contributions can be made until the federal income tax return filing due date.

- The plan must be established by December 31st.

Defined Benefit Plan

- The Defined benefit plan is for high-income self-employed individuals, professionals, and small business owners.

- This plan has significantly higher deductible contributions in comparison to other retirement plans. These plans are not subject to the limit of 25% of compensation as are SEP and 401(k) plans.

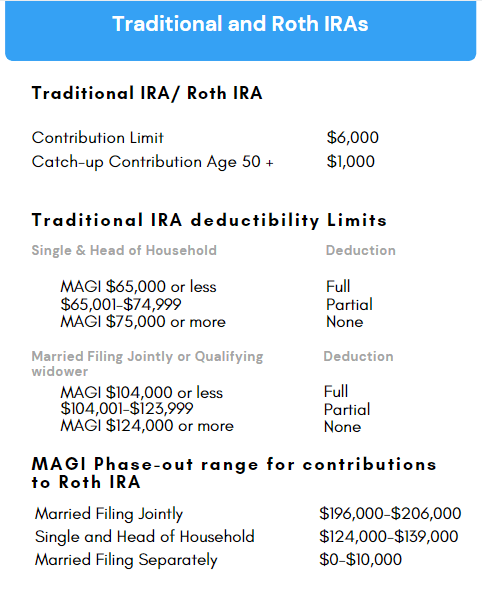

Traditional IRA vs Roth IRA

Traditional IRA

- Tax-deferred growth

- Contributions are tax-deductible, “before-tax dollars”

- Withdrawals are taxed as ordinary income

- Withdrawals prior to age 59 1/2 result in a 10% penalty

- Tax deduction limits are based on your Modified Adjusted Gross Income (MAGI)

- No age limit for contribution

- The contribution must be from earned income

- The contribution deadline is the due date of the individual income tax return

Roth IRA

- Tax-free growth

- Contributions are not tax-deductible, “after-tax dollars”

- Withdrawals are tax-free

- Contributions can be withdrawn early tax-free and penalty-free, earnings may be taxable

- Contribution limits based on your Modified Adjusted Gross Income (MSGI

- No age limit for Contribution

- The contribution must be from earned income

- The contribution deadline is the due date of the individual income tax return

Traditional 401(k)/403(k) vs Roth 401(k)/403(k)

Traditional 401(k)/403(k)

- Tax-deferred growth

- Contributions are tax-deductible

- Withdrawals are taxed as ordinary income

- Withdrawals prior to age 59 1/2 result in a 10% penalty

- No income limits for contributions

- Participant must be employed

- The contribution deadline is December 31st

Roth 401(k)/403(k)

- Tax-free growth

- Contributions are not tax-deductible

- Withdrawals are tax-free

- The earnings portion of an early withdrawal is taxable and may be subject to a 10% penalty

- No income limits for contributions

- Participant must be employed

- The contribution deadline is December 31st

Roth Conversions

Converting to a Roth IRA from a traditional IRA would make sense if you’ve experienced a loss of income (lowering your tax bracket) or if your retirement accounts have decreased in value.

Charitable Giving

Taxpayers who are age 70 1/2 can make Qualified Charitable Distribution (QCDs) of up to $100,000 per year (or $200,000 for married couples) directly from IRA accounts by donating them to an eligible charitable organization(s). Eligible taxpayers can take advantage of QCDs even though the CARES Act eliminated the requirement for required minimum distributions for 2020.

Saver’s Tax Credit

The Savers Credit, also known as the Retirement Savings Contributions Credit, gives a tax break to those who contribute to a retirement plan. The maximum credit amount is $1,000 ($2,000 if married filing jointly). It is a non-refundable tax credit. It can be claimed for contributions made to 401(k), 403(b), 457 plan, Simple IRA, or SEP IRA. In 2020, the adjusted gross income limit for the saver’s credit is $65,000 for married couples filing jointly, $48,750 for heads of household, and $32,500 for married individuals filing separately and for singles.

SECURE Act

The SECURE (Setting Every Community Up for Retirement Enhancement) Act passed by Congress in December 2019, includes a broad range of provisions that bring significant changes to retirement legislation.

- Repeal of maximum age for traditional IRA contributions There is no longer an age limit for IRA contributions for the tax year 2020 and beyond, provided they have earned income.

- Increased in the RMD age The starting age for Required Minimum Distributions (RMDs) was increased to age 72 for individuals born after 1949.

- Qualified birth or adoption distributions Allows penalty-free early retirement account withdrawals for birth or adoption, up to $5,000 within one year of occurrence.

- Inherited IRAs It eliminated “Stretch IRA”. Most Beneficiaries of Inherited Retirement Accounts are required to fully withdraw assets within 10 years. Exceptions apply to certain account beneficiaries, such as spouses, beneficiaries who are disabled, heirs within 10 years of age of the original account owner.

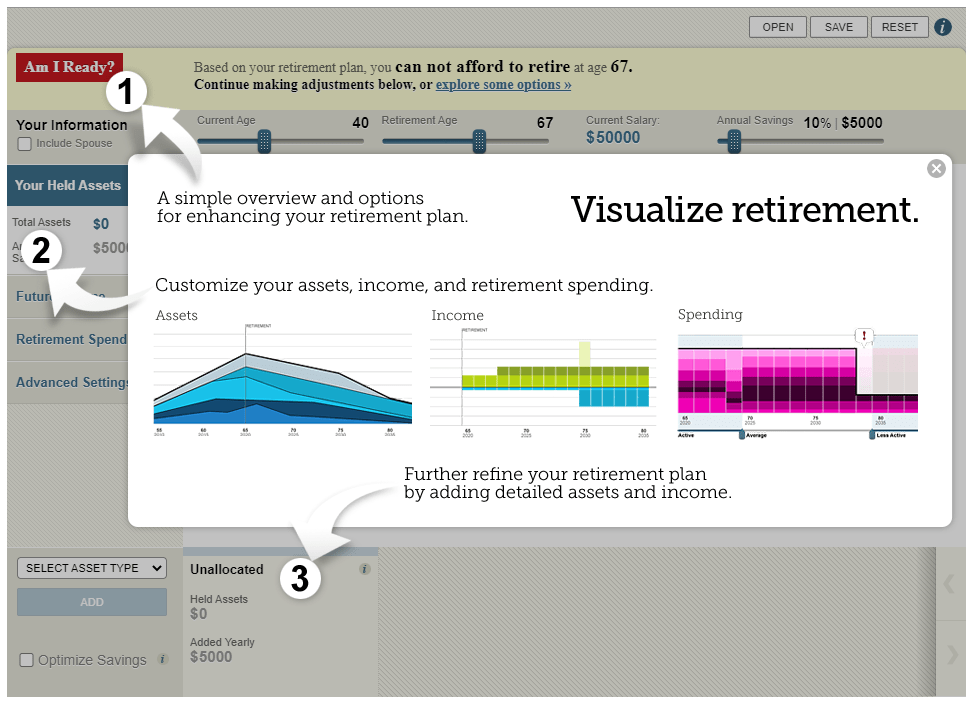

Are You On Track for Retirement?

Click to view online Retirement Planner